Young Canadians are holding fast to the dream of buying a home, even as overall rates of ownership are falling sharply, according to a new poll released by Scotiabank Tuesday.

The polling shows a steep decline in young homeowners over the past three years as housing unaffordability issues dogged would-be buyers. Some 26 per cent of Canadians aged 18 to 34 own a home today, down from 47 per cent in 2021, according to the poll.

At the same time, 29 per cent of respondents in that age group reported they were living at home with parents or family, up nine percentage points from three years ago. The number of renters was similarly higher among youth, up to 43 per cent from 29 per cent in 2021.

Home ownership plummets? That’s not what I’ve heard. Corporations seem to own every home they can buy, and they buy them in bulk.

In Montreal, about 0.1% of the people own about 30% of the properties. Most of them are rich property investors. Many of which are real estate agents, too. They own the market.

As far as large cities in Canada go I was under the impression Montreal is among the more affordable ones too, so for the most part it only gets worse.

Yeah, it does.

Obviously houses are owned by someone, either people, corporations, public entities. Home ownership usually refers to the share of people owning the homes they live in.

I was being sarcastic. Obviously they aren’t talking about corporate home ownership.

I would love it if renting was just banned entirely. Just play the stock market with your extra cash, homes should not be an investment/traded around. People need a place to live. I hope people realize that a shoebox of a condo isn’t worth $1M and theres a massive correction back to more realistic valuations. its just stupid now.

I don’t think renting should be completely banned, but it shouldn’t be profitable. Property value appreciation already makes money.

That’s silly. Rent controls, an aggressive rental board, expansion of non-market housing, strong tenant unions, and the abolition of restrictive zoning, these are the things we actually need.

Unless we are also abolishing wage slavery and private property, in which case, sure ban renting.

I don’t really want to go through the process of buying a home every few years until I settle down.

Some 26 per cent of Canadians aged 18 to 34 own a home today, down from 47 per cent in 2021, according to the poll.

Not only that, but it sounds like homebuilders have been decreasing housing starts for several years, which seems counterintuitive if one has high housing prices.

TORONTO, April 4 (Reuters) - Canadian homebuilders are expected to dial back new construction for a third straight year in 2024 as elevated borrowing costs reduce the appeal of starting projects, Canada’s national housing agency said on Thursday.

Here’s my off-the-cuff understanding of the situation. I have not been closely following it.

In the wake of the global financial crisis, it looks like Canada cranked the central bank’s interest rate way down.

Shortly after Canada started bringing them back up, COVID-19 hit, and Canada slammed rates back down again. It wasn’t until inflation started to rapidly rise in mid-2022 that Canada started bringing them back up, at which point, Canada had had low interest rates for over a decade.

https://tradingeconomics.com/canada/interest-rate

My understanding is that one effect of running low interest rates is to create asset price bubbles. It’s cheap to borrow money, so people borrow a lot of money and dump a lot of it into housing, which blows the price of housing way up.

This has led to what is believed to be a housing price bubble considerably worse than the one that the US hit:

https://en.wikipedia.org/wiki/Canadian_property_bubble

In 2023 Canada’s nonfinancial debt exceeded 300% of GDP and household debt surpassed 100% of GDP, both higher than the levels seen in the United States before the 2008 global financial crisis. Canada’s housing investment as a percentage of GDP ratio peaked at 8.9% in 2022, whereas the US, at the peak of their housing bubble, only reached 7% in 2006.

This happened because it was cheap to borrow a lot of money under Canadian policy, and so what people did – looking at the rapid increase in Canadian housing prices – was to borrow a lot of money and buy housing with the expectation that it would continue to rise, and that by doing so with a lot of borrowed money, they’d increase their gains:

Investor activity (measured as the percentage of non-owner-occupied homes) increased both housing price appreciation and price collapse during the 2007–2008 financial crisis. Investor activity peaked in 2005, with over 29% of new mortgages in Las Vegas taken out for investment properties. At this time, 15% of mortgages across the US were for non-owner-occupied homes.[80] In 2020, in Toronto, 21% of all housing, and 56% of condos were investor owned. In Vancouver, nearly 48% of condos, and 33% of all housing was owned by investors.[81] Across Canada, 1 in 5 homes were investment properties. Investors were found to be increasingly crowding out prospective first-time buyers in a 2024 analysis.[82]

With Canada finally bringing interest rates up, house builders – expecting that they’re going to have a hard time selling houses – are having a hard time borrowing money to build more houses, so they pulled back on new construction. At that point, you have a lot of people with borrowed money that have soaked up a lot of housing, expecting it to continue to rise.

So I’d expect Canadian house prices to begin falling. When that happens, suddenly that investment in housing that seems like a really great idea because you’re using borrowed money to increase gains becomes a really bad idea, and you want to get out. But…you can’t sell that housing to anyone. So you potentially have a lot of people who want to dump housing all at once, which causes a bubble to pop.

Normally, when a buyer gets a mortgage, they have to make a down payment, though in the runup to the global financial crisis, a lot of US mortgage lenders were issuing a lot of mortgages with no money down. The purpose of this is to shield the lender from risk (and reduces interest rates from the borrower). Someone with a mortgage has $E equity in a house, the part that they own, and then $M that they borrowed from the bank. If someone defaults on their mortgage, because the house was pledged as collateral, then the lender can seize the house and sell it on the market to recover their $M, with their $M getting priority over the borrower recovering their $E.

Normally, that down payment is chosen by a mortgage lender large enough that even if house prices fluctuate and the price drops shortly after sale, the money can be recovered by the lender, so the risk is mostly on the borrower.

However, if house prices rapidly collapse far enough, then it may be that a house price isn’t high enough for a lender to recover the money they lent. That is, after sale prices go “underwater”, such that the borrower has lost all their equity and then the lender can’t even recover their loan if they seize the house and sell it, then the lender faces risk that the borrower will simply default on the mortgage, and the lender will not be able to fully recover the money they lent on the house.

That can lead to mass defaults by borrowers, which is what happened in a number of places in the US when housing prices rapidly dropped, which led to houses being seized and placed on the market, which further drove down housing prices.

My vague recollection – and I have not followed the Canadian housing situation closely; this is going from my memory of comparative housing policy back around the global financial crisis – is that Canadian mortgages are all recourse. In a minority – but important minority – of US states, mortgages are non-recourse (at least on the primary mortgage; this doesn’t apply to secondary mortgages, HELOCs, etc, at least in California, by my way of recollection). What that refers to is whether the lender has recourse if a buyer defaults on their mortgage. That is, can they try to seize other personal assets, garnish income, have some other forms of trying to recover their money in a default.

That will probably tend to make it less-likely for Canadians to walk away from debts…but I don’t think that it makes lenders immune. That is, if someone files for personal bankruptcy – which might be a good idea if they don’t have a lot of assets outside the house and they have borrowed an enormous amount to buy a house that is worth far less than they paid for it – I’d guess that the lender probably has no recourse, though I haven’t gone researching Canadian law on the matter. Or if someone is an overseas buyer – something that Canada has recently severely restricted – it may be hard to go after their other assets to recover loss if they default even if they don’t declare bankruptcy.

In general, Canada’s less-borrower-friendly, more-lender-friendly laws probably means that the Canadian banking system won’t get into as much risk of banks getting clobbered as the US, even if a bubble pops. But that doesn’t mean that people who buy houses can’t be considerably-worse-off than they otherwise would have been.

Another factor is that in the US, the most-common type of mortgage is a 30-year fixed-rate mortgage. As interest rates fluctuate, they don’t affect people who already have a mortgage rate locked in. That does mean that if interest rates rise, they may not be able to easily move; labor mobility will take a hit, which isn’t good. But they can probably continue to pay the mortgage on their existing home, as long as their income continues. Canadian borrowers, as I understand it, normally need to refinance their mortgage each five years, so their mortgage payments are affected by current interest rates. If interest rates rise, as they have their payments will also rise starting at some point in the next five years. Canadian interest rates have recently risen quite considerably.

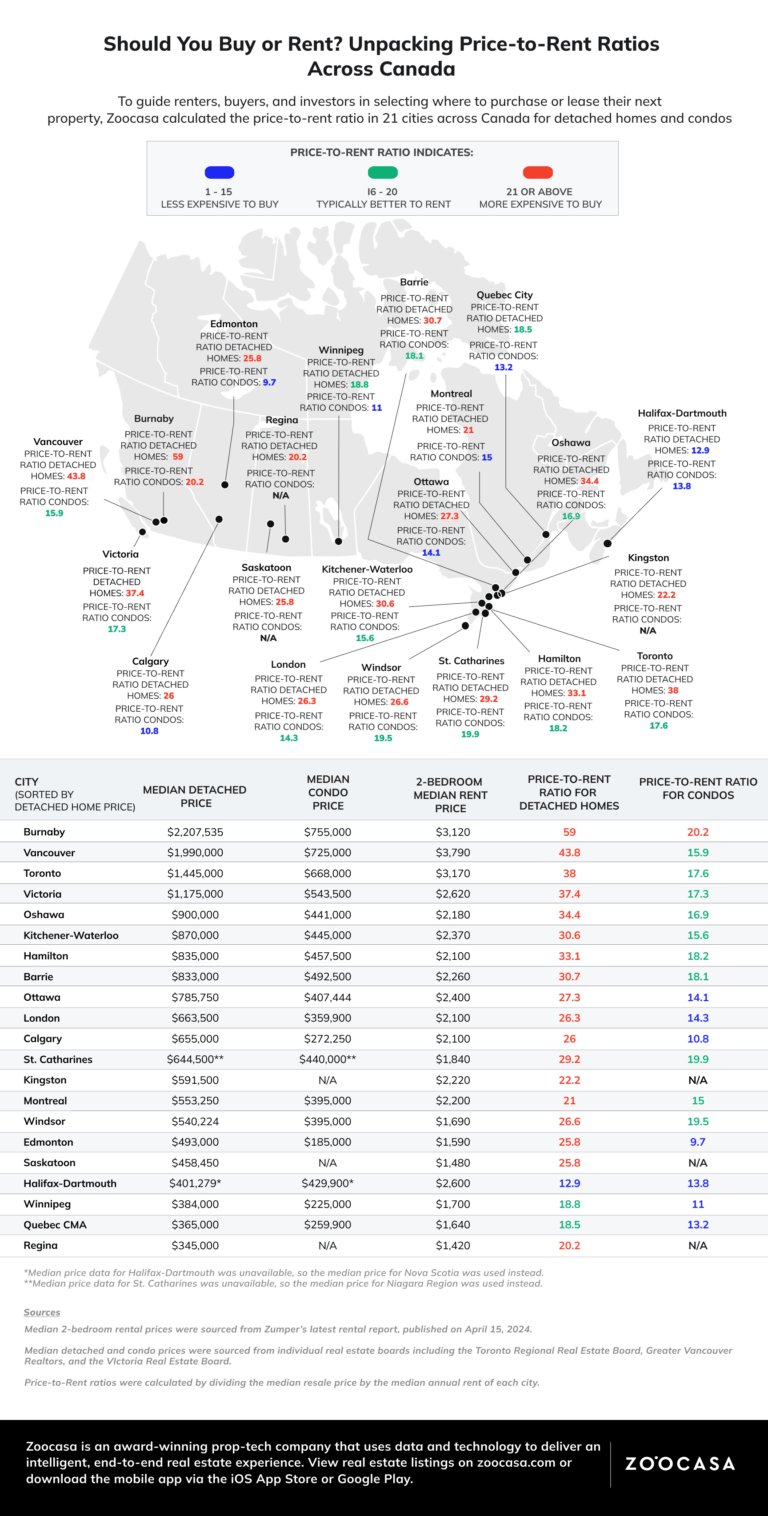

One cause of high housing prices is if there just isn’t enough housing supply out there at all, like, construction can be constrained by zoning laws and such. Another is that the supply of housing is out there, but people are determined to purchase rather than renting. Potentially each is true to some degree, but a way to determine whether people are irrationally bent on purchasing is to look at the price-to-rent ratio. This, as a rule of thumb, is generally expected to hover in a vaguely-fixed range.

kagis for Canadian price-to-rent ratio data

https://www.zoocasa.com/blog/price-to-rent-ratios-across-canada/

https://www.zoocasa.com/blog/wp-content/uploads/2024/05/Townhouse-downpayment-1-1-768x1516.png

Based on that, the price-to-rent ratios in almost all of Canada are relatively high for detached homes. That means that at least part of the situation is people buying when they probably should be renting in terms of expected financial return. Unless what a Canadian is looking to live in is a unit in a multiunit building, I expect that it’s probably a good move for a Canadian to rent right now, avoid exposure to the real estate market. One would want to have their assets in something other than equity in single-family home real estate, like stocks or bonds or suchlike.

Ah, the Canadian housing bubble Wikipedia article talks about some of the points I raised:

https://en.wikipedia.org/wiki/Canadian_property_bubble

Risks

Canada is a nation heavily dependent on the real estate industry which accounted for roughly 14% of its GDP in 2020[126] and over 20% in 2023.[127] There is a high risk that if investor sentiment changes, buyer demand may drop significantly, triggering a vicious cycle of prices declines that snowball.[128] Canadians hold increasing mortgage debt (almost $2 trillion in June 2021,[129] $2.16 trillion residential in 2023[130]) while unemployment rose and net employment fell in 2024.[131]

That “snowball” is referring to a bubble popping. And this also mentions the five-year mortgage factor:

Short-term fixed-rate mortgages are dominant in Canada,[132] typically with the interest rate locked in for five years. This contrasts with the United States, where most homeowners hold long-term fixed-rate mortgage contracts. If the reset rate in five, ten, or fifteen years is higher than in the past, there will be a large risk of default for Canadians with high amounts of debt. A July 2017 report noted that uninsured mortgages represent the greatest risk to the financial industry.[133] A decreasing number of Canadian mortgages are backed by insurance, from over 60% in 2012[134] to less than 22% in 2022.[135] Drops in home prices could cause homeowners to owe more on their mortgages than the house is currently valued, which is known as negative equity.[136][128]

The interest rates are already falling and most have weathered the storm. The pressure needed to pop the bubble is being relieved so I doubt it’s going to blow up. Rather I think we’ll see a long sideways movement.

Move to the prairies folks. Vancouver has no place to build new homes. Montreal is an island. Toronto has real and artificial constraints keeping the sprawl contained.

Move to Winnipeg. Regina. Edmonton. Whatever. Own a home like it is 1965. If they’re still too expensive, move to an even smaller city. The jobs are available.

How’s the social scene for a young-ish single person?

Depends on the city. And who you are. I’m a big white dude with a geophysics degree so the circles I run in tend to be coloured by that.

I lived in Edmonton a decade ago, and it was great as a young professional. However, because the city is full of oil money, you really have to work hard to impress anyone with your career there. They’re all like “yeah, whatever, everyone at this bar is throwing down $100s and you’re just one of them assholes”, so you have to be pretty self-aware to date there. But going to a “drink and draw” event at an art gallery will work wonders ;)

Currently in Winnipeg. The arts scene here is great. Met my long term partner here (online dating during COVID, even – “do you want to go on a socially distant walk in the park together?”). She is more hipster than I so I basically ride her coattails now in the art scene. We went “power couple” for our first two years – two houses because that’s how affordable it is.

I have lived, worked, or studied in seven provinces and three territories now. I joke with my friends from elsewhere that when I moved to Winnipeg, I bought a garage and it came with a free house. My quite decent three bedroom, finished basement, double garage was $286k.

Well, it’s cold in winter and very flat topographically, but whatever – I lived in Yellowknife so this is nothing ;)

Photo just outside Winnipeg on the frozen lake – hiking to find cool ice ridges. Just gotta lean into winter :)

Global News - News Source Context (Click to view Full Report)

Information for Global News:

MBFC: Left-Center - Credibility: High - Factual Reporting: High - Canada

Search topics on Ground.News

https://globalnews.ca/news/10836339/young-canadian-home-ownership-affordability/

{kind=link}